Forestry Update Amidst COVID and Trade Disruptions

Forestry Update Amidst COVID and Trade Disruptions

Published on July 28, 2020

It is difficult to determine how much of the hardwood log and lumber pricing decline is related to the COVID situation or even the trade war with China. The pricing observed from 2017 through mid-2018 was in part largely due to the higher pricing from the export market of hardwood logs and green lumber to China stimulating the market, alongside steady domestic demand. That was until the trade war started July, 6th 2018 when tariffs were placed on China for its alleged unfair trade practices. Following the tariff announcement, purchase orders for US hardwood logs and lumber almost immediately decreased and prices have continued to drop over the 2-year trade conflict period. Certainly, COVID has not helped. The industry was classified as essential, so it did not have to shut down as result of the state’s executive orders. That would have certainly caused some issues with the markets. Hardwood mills and plants are struggling with trying to keep their workforces healthy through this pandemic. Some mills claim that orders are slow and prices are low and some others are nervous about making future production commitments for fear of employees getting sick and requiring a shutdown to deal with the situation. In summary, uncertainty is the norm which for any sector is a significant problem.

Despite what you may have heard about all the home remodel work going on during the COVID-19 pandemic this is not translating to an increase in log and lumber consumption or stability in pricing. Table 1 below shows that statewide average pricing decreased 17% across all species and grades for hardwood logs delivered to the mill during the quarters 1&2 of 2018, 2019, and 2020. Generally, the price collapse was worse for higher quality logs than lower quality logs. The worst hit are ash down 20-30%, cherry 40% and red oak off 20-30%. The latter is very important as Kentucky has a significant volume of red oak across the state. Its reduction has caused many timber stands to decrease in overall value and make many landowners shy away from selling timber. However, the reduction in available supply has not offset the decreased demand and price. Soft maple (red maple) is the only species that has increased in value since 2018 and it is not an extremely valuable or high volume species.

Table 1. Delivered Log Pricing Comparison for 1&2 Quarters of 2018,2019, and 2020 in $MBF

| Species | Quality | 2018 1&2Q | 2019 1&2Q | 2020 1&2Q | % Change from 1&2Q 2018 to 1&2Q 2020 |

|---|---|---|---|---|---|

| Ash | High | $664 | $675 | $482 | -27.3% |

| Ash | Low | $267 | $274 | $276 | 3.4% |

| Chestnut oak | High | $1,121 | $1,138 | $1,017 | -9.2% |

| Chestnut oak | Low | $283 | $318 | $309 | 9.2% |

| Cherry | High | $840 | $745 | $493 | -41.2% |

| Cherry | Low | $286 | $302 | $270 | -5.3% |

| Hickory | High | $552 | $514 | $464 | -15.9% |

| Hickory | Low | $254 | $272 | $260 | 2.5% |

| Hard maple | High | $840 | $858 | $760 | -9.4% |

| Hard maple | Low | $295 | $316 | $306 | 3.9% |

| Red oak | High | $827 | $685 | $543 | -34.2% |

| Red oak | Low | $312 | $288 | $310 | -0.5% |

| Soft maple | High | $452 | $536 | $490 | 8.4% |

| Soft maple | Low | $213 | $265 | $278 | 31.2% |

| Walnut | High | $1,929 | $2,046 | $1,943 | 0.8% |

| Walnut | Low | $435 | $589 | $436 | 0.4% |

| White oak | High | $1,183 | $1,127 | $1,085 | -8.3% |

| White oak | Low | $315 | $327 | $323 | 2.8% |

| Yellow-poplar | High | $566 | $592 | $532 | -5.9% |

| Yellow-poplar | Low | $244 | $283 | $252 | 3.6% |

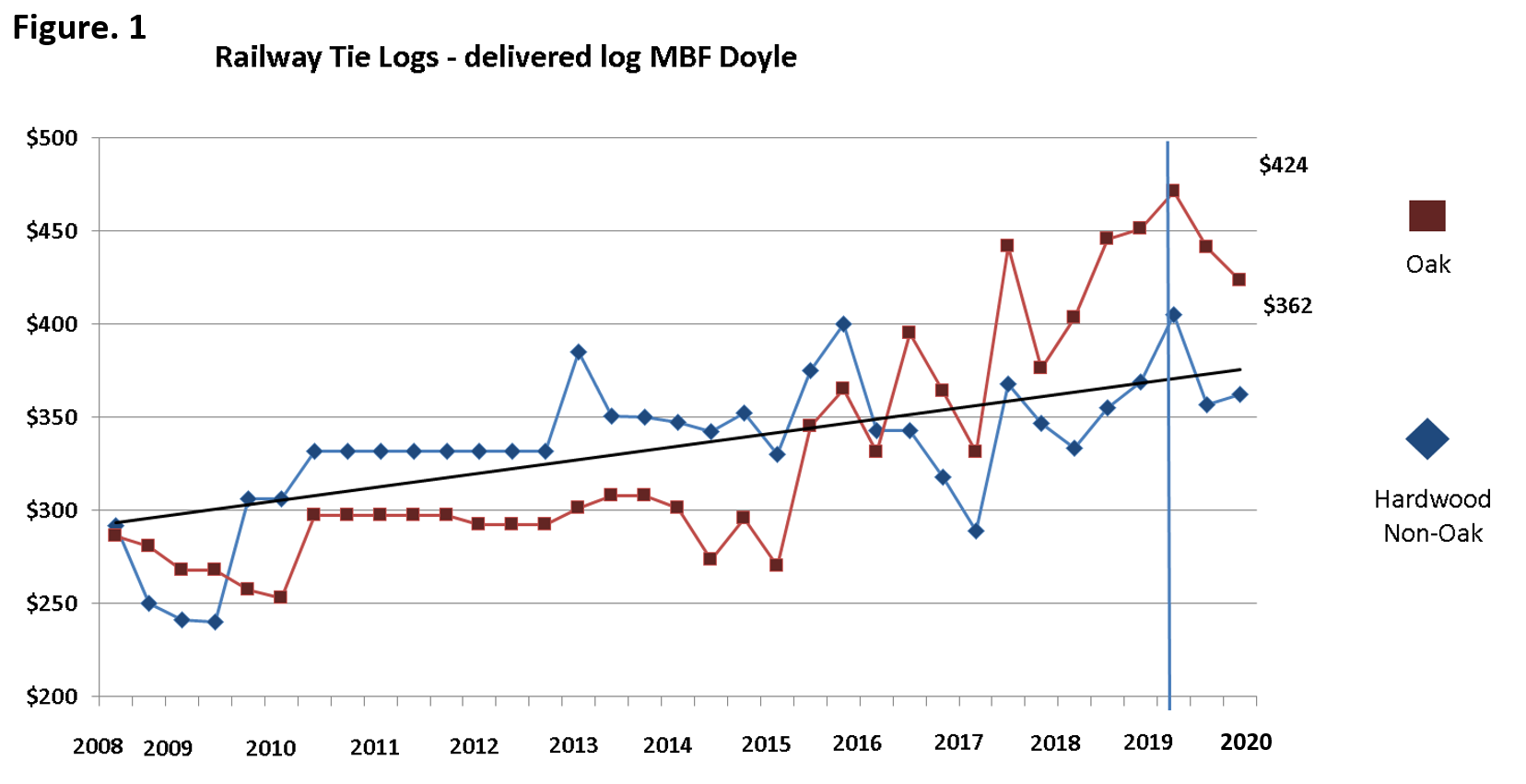

There are areas of the wood industry that are not complete doom and gloom. Moulding and Millwork, railroad ties, and cooperage all seem to be holding their own, but certainly not booming. All three have shown some decline in 2019 and no improvement in 2020. The positive news is they just have not fallen as much as the rest of the industry. Railroad tie logs are an important market for Kentucky as every woodland owner and acre of woods has this material. Figure 1 below shows the price trend for oak and non-oak ties.

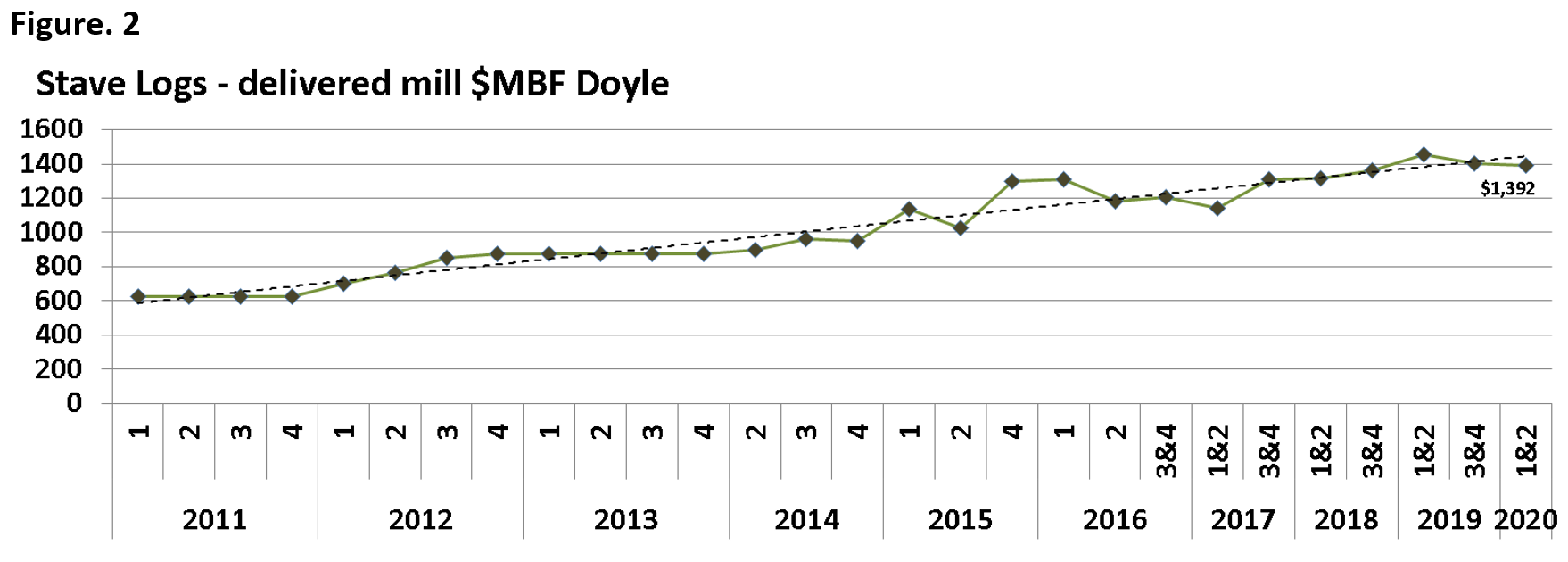

White oak is directly impacted by the cooperage industry. Figure 2 below shows the statewide pricing trend for white oak stave logs.

The lumber side of things are not much better. On average since January of 2019 hardwood grade lumber has lost 27% of its value and since January of 2020 lumber values are down 4.3%. These values were calculated from the top-selling lumber species in the state. White oak lumber markets for example fell 13% in average value in 2019 but have remained flat in 2020 so far. With the values falling as much as they have that puts significant pressure on the mills to stop buying logs or have quotas on how much loggers can deliver to them. Both drive down the log and timber prices. A few mills have even opted to shut down production indefinitely until markets improve. As demand for timber in the US and worldwide decreases, inventories of lumber and finished products across the industry are increasing. In addition, the mills are having to deal with closed or shrinking markets for residuals they produce such as chips or pallet materials. Kentucky had two paper mills, that many sawmills and other forest industries sold chips to, temporarily shut down production in 2020, creating huge concern for the sawmills. One of those paper mills still remains idle. Residuals such as chips and bark are not a high-profit item for sawmills however, sawmills have only so much storage capacity and once full it becomes a real problem for the mills to process logs. The same can be said for low-grade pallet materials.

Sources:

Hardwood Market report- https://hmr.com/

Kentucky Growing Gold and Delivered Log Price Report- Kentucky Division of Forestry, Forest Resource Utilization and Marketing (FRU) program

Author(s) Contact Information:

Chad Niman | Primary Forest Products Specialist | chad.niman@uky.edu

Bobby Ammerman | Extension Associate of Secondary Wood Industry | bammerma@uky.edu

Jeff Stringer | Chairman, Department of Forestry and Natural Resources | stringer@uky.edu