Interest Rates and Grain Storage

Interest Rates and Grain Storage

For the 2023/24 marketing year, higher interest rates will negatively impact producers' costs for holding grain in storage, especially for producers utilizing operating loans. This article examines the operating loan interest cost of storing grains at different interest rates and lengths of time and how to calculate operating loan interest costs when the grain is stored. The article also provides charts to depict the change in operating loan interest cost of storing corn, soybeans, and wheat. For example, an increase in the interest rate from 4% to 10% will increase the storage costs of corn stored for five months by 162.5% or $0.13/bushel.

The Federal Reserve began increasing the Federal Funds rate in February 2022 to combat inflation. When the Federal Reserve raises the Federal Funds rate, the prime rate increases. The prime rate is used as a reference interest rate for many types of loans, including operating, term, and credit card loans. On July 27, 2023, the prime rate reached 8.5%, the highest since 2001. Speculators believe further increases of 0.25-0.50% will occur before the end of the year. Kentucky lenders have recently mentioned operating loan rates of 9.5%, indicating that the operating loan rates could reach 9.75-10.00% before year-end.

Higher interest rates impact every aspect of a farming operation. Still, as they pertain to marketing strategies, they are likely most impactful on producers using operating loans to hold grain in storage. Typically, operating loans are variable interest rate, meaning they are not fixed but increase when the prime rate changes; however, some lenders have started offering fixed-rate operating loans to provide customers with cost certainty. Operating loans are used to pay for inputs until grain can be sold and the operating loan paid back. There is an interest cost for holding grain in storage compared to selling at harvest and paying down operating loans. Grain in storage typically allows producers to increase profit through marketing strategies that utilize market or basis carry. However, the operating loan interest costs need to be accounted for when interest rates are elevated.

The operating loan interest cost on a dollar-per-bushel basis can be calculated by multiplying the harvest price by the interest rate and dividing the number of months the crop is stored by 12. For example, a producer that holds corn harvested in October until March (5 months), has an operating loan interest rate of 10% interest and is expecting a harvest price of $5.00/bushel would have operating loan interest costs of storage of $5.00 × 0.10 × (5/12).

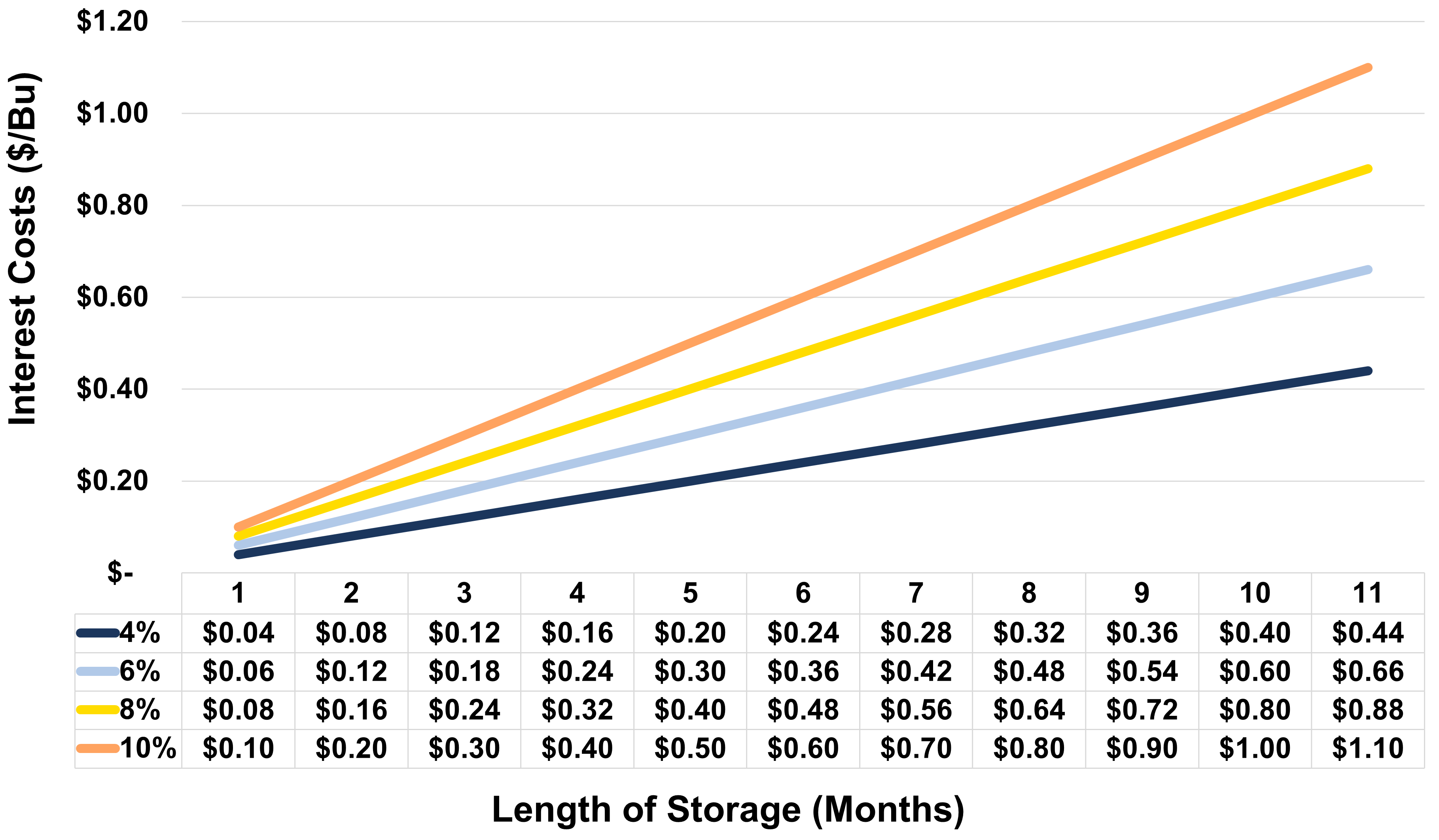

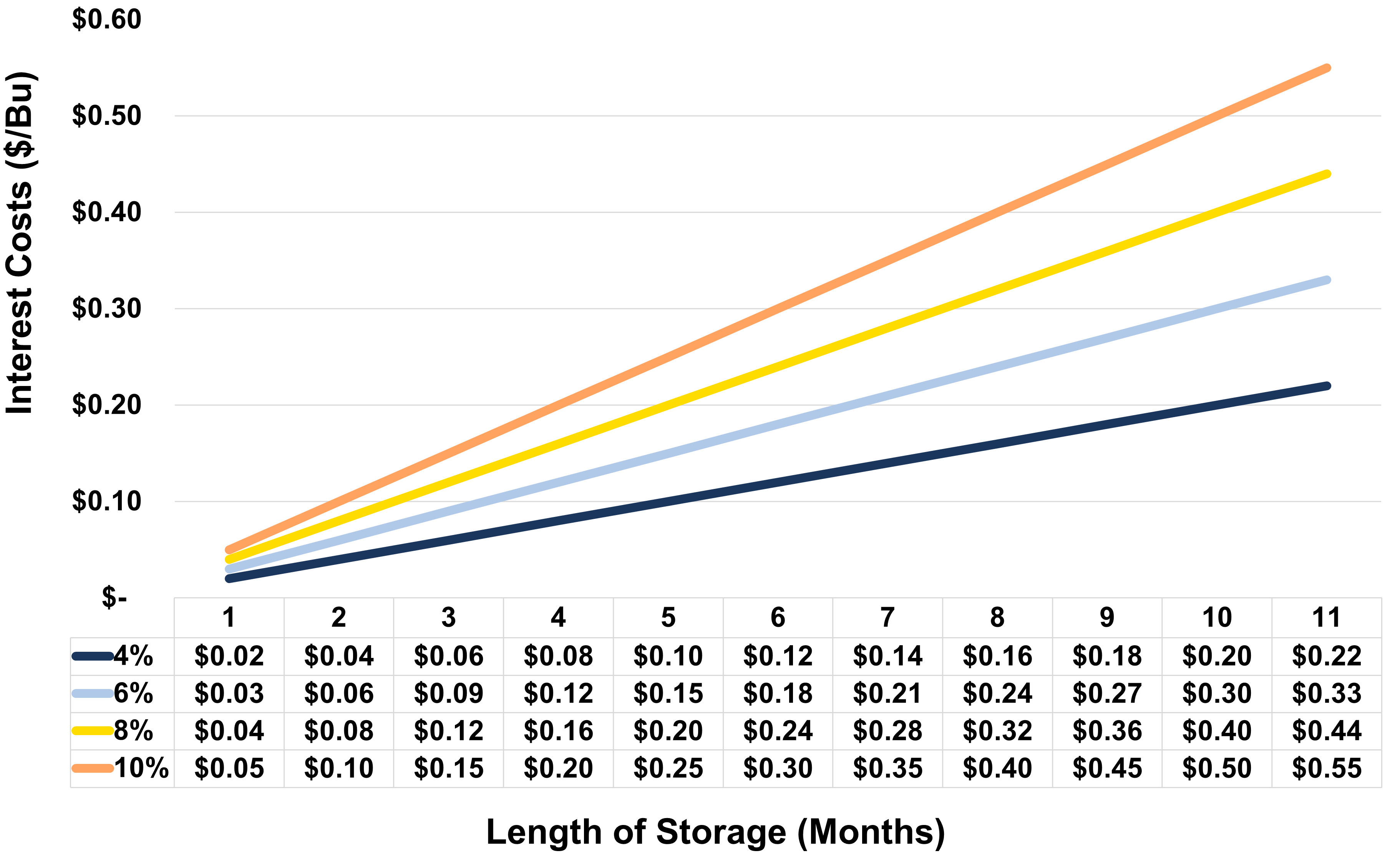

Figures 1, 2, and 3 show the impact of the number of months of storage and interest rates on corn, soybeans, and SRW wheat operating loan storage costs. Harvest prices are assumed to be $5.00/bu for corn, $12.00/bu for soybeans, and $6.00/bu for SRW wheat. The storage costs increase the longer grain is stored. Additionally, costs increase as the price of the commodity increases, i.e., interest costs are higher for soybeans than corn or SRW wheat.

The table at the bottom of each chart can be used to estimate increased operating loan interest costs for grain held in storage due to climbing interest rates. Following our previous example, if corn is harvested in October for March delivery (5 months) and the interest rate is 4%, operating loan interest costs of storage for $5 corn would have been $0.08/bu. When the rate increases to 10%, closer to current rates, the operating loan interest costs of storage are $0.21 per bushel. This result indicates an increased operating loan interest cost of $0.13/bu ($0.21 minus $0.08), a 162.5% increase due to a 6% increase in interest rates.

In conclusion, high-interest rates increase the storage costs for producers holding grain via an operating loan, affecting each operation's bottom line and potentially negating the price benefits of storage. Storage costs are rising with interest rates which should be accounted for in your grain marketing decisions. It is worth noting that the impact of higher rates could be mitigated/stopped by paying your operating loan off early or using cash reserves instead of loans, respectively.

Figure 1: Impact of Interest Rate Increases on Corn Storage Costs

Note: Costs do not account for physical storage costs such as bin depreciation, transport, drying, etc.

Figure 2: Impact of Interest Rate Increases on Soybean Storage Costs

Note: Costs do not account for physical storage costs such as bin depreciation, transport, drying, etc.

Figure 3: Impact of Interest Rate Increases on SRW Wheat Storage Costs

Note: Costs do not account for physical storage costs such as bin depreciation, transport, drying, etc.

Recommended Citation Format:

Gardner, G. "Interest Rates and Grain Storage." Economic and Policy Update (23):8, Department of Agricultural Economics, University of Kentucky, August 29th, 2023.

Author(s) Contact Information: